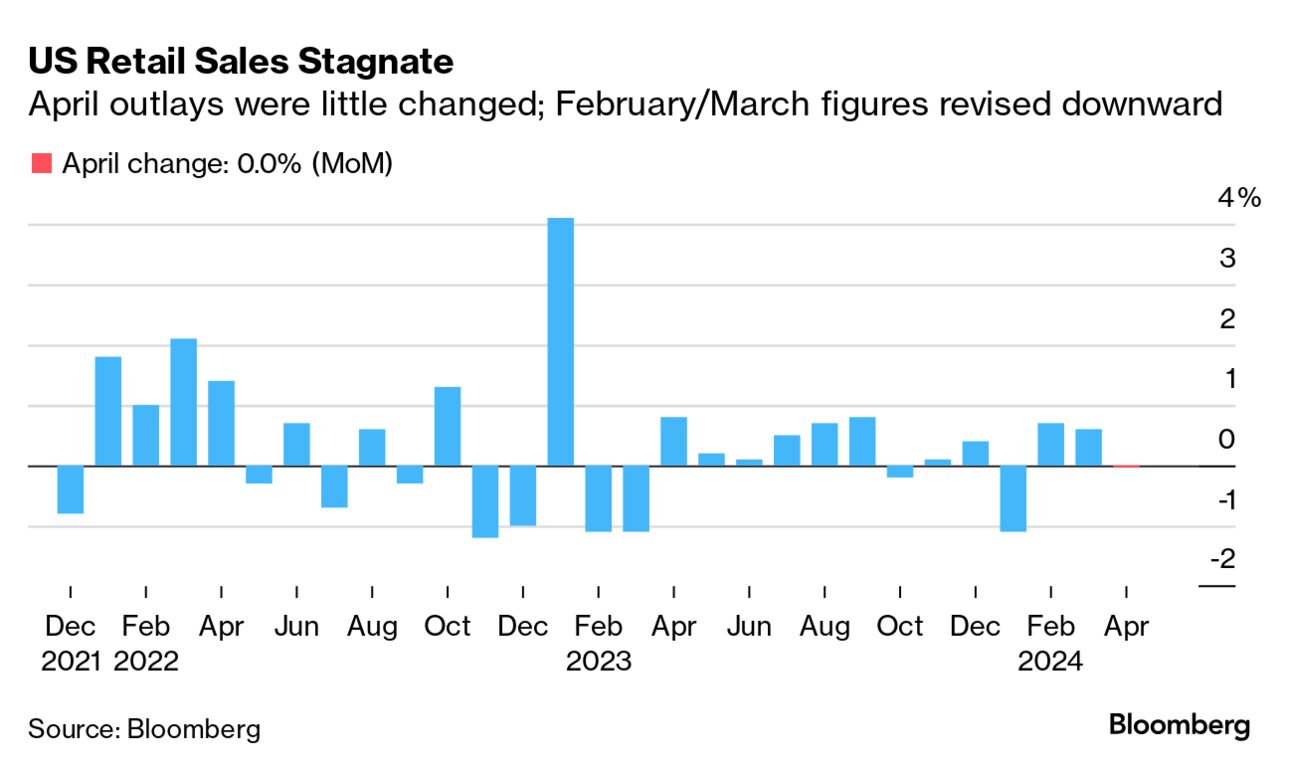

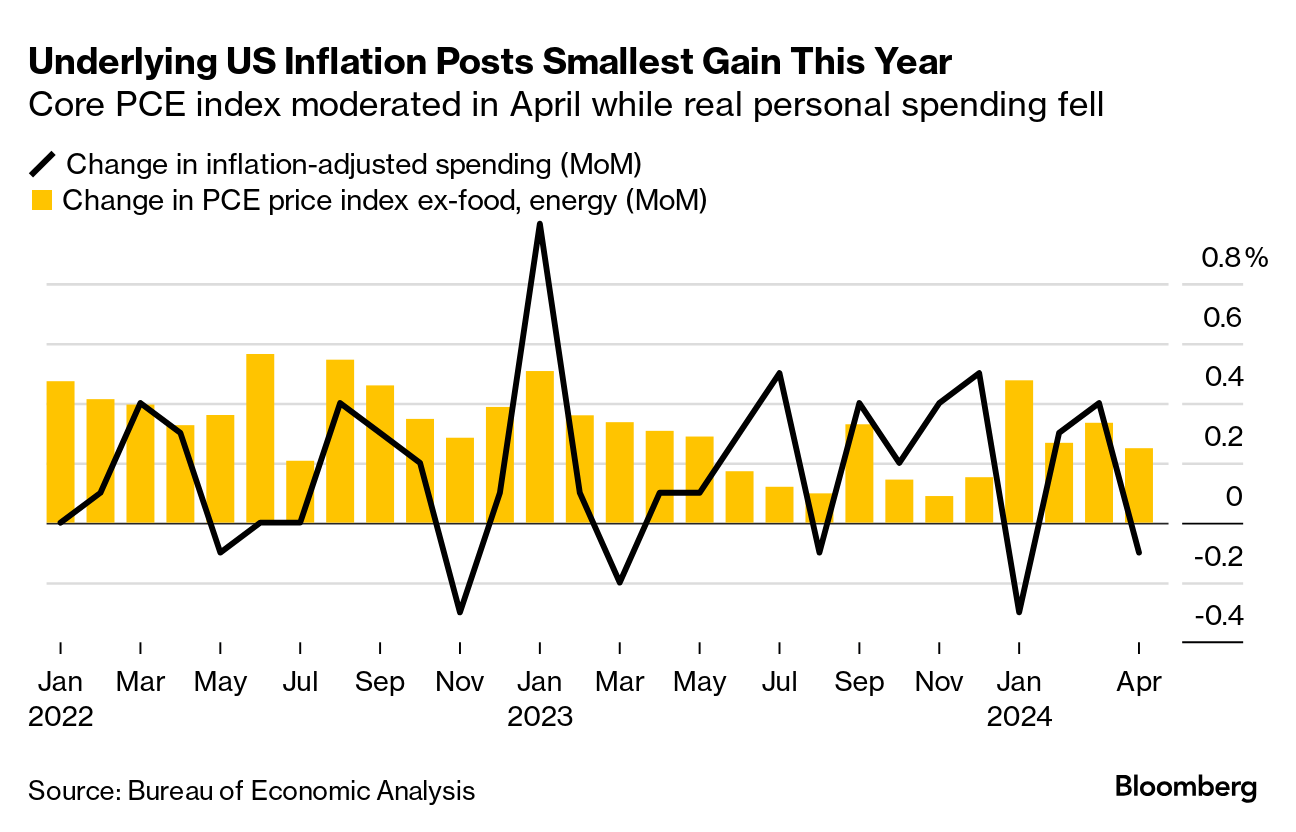

US consumers have powered through the worst bout of inflation in more than a generation, supply-chain woes and dire labor shortages. They may now be flagging. Data out on Friday corroborated evidence that spending kicked off the second quarter on a soft note. Personal consumption rose just 0.2% in April from the previous month, and was actually down when taking inflation into account. That's after a core gauge of retail sales, out earlier in May, had shown a contraction. Spending essentially has to come from one of three places: earnings, savings or credit. And all three metrics are suggesting a slowdown. - Real disposable income — that is, after taxes and inflation — declined in April for the second time in three months, after a scant 0.1% rise in March.

- The saving rate now stands at a 16-month low as households have mostly exhausted the extra pile of cash they squirreled away during the pandemic.

- Evidence suggests more households are getting tapped out in terms of credit, with credit-card delinquency rates on the rise, albeit still lower than pre-pandemic. About one in six credit card users are using at least 90% of their available credit.

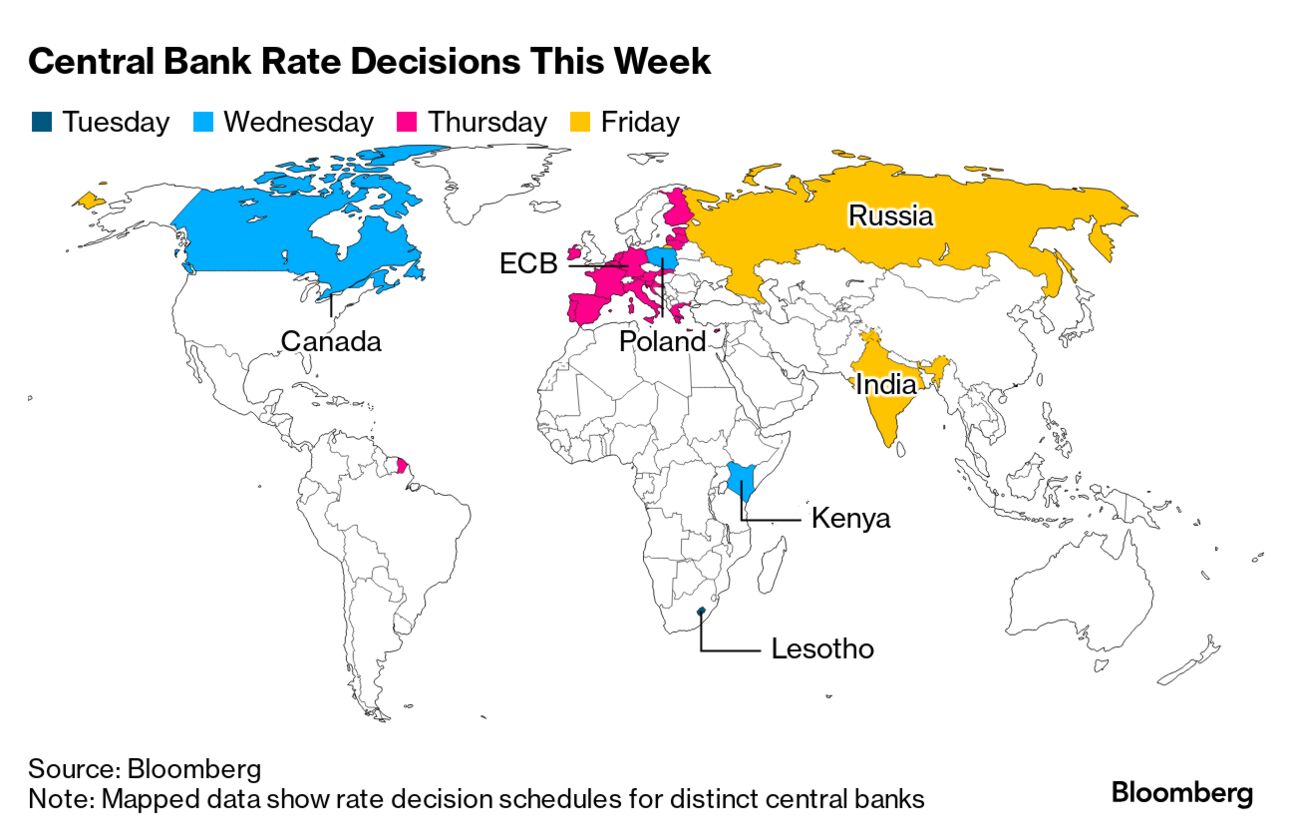

"Slower labor market momentum will continue to limit income growth and push more families to exercise spending restraint amid reduced savings buffers and higher debt burdens," Gregory Daco, EY chief economist, said in a note Friday. "Factoring increased price sensitivity, household spending momentum will gradually cool." Demand for workers has come down from its pandemic peaks, meaning employers aren't hiking pay as quickly anymore. Wages and salaries advanced 0.2% in April, the smallest gain in five months, data out on Friday showed. The May jobs report, due next Friday, will offer more insights into the direction of the labor market. But for now, second-quarter spending is shaping up to be a down-shift from the post-Covid go-go years. The European Central Bank could open the door to a weaker euro on Thursday as its first rate cut of the cycle puts the region on a divergent policy path from the US. With a quarter-point reduction all but certain, officials will finally embrace a widening in the difference between borrowing costs on either side of the Atlantic, the implications of which they've discussed for months. See here for the rest of the week's economic events. Inflation may not return to the US central bank's 2% target until mid-2027, according to fresh research from Federal Reserve Bank of Cleveland. That's because the inflationary impact of pandemic-era shocks have largely resolved — think supply-chain woes and dire labor shortages — and that disinflationary process has largely ended. Meantime, the remaining forces that are keeping inflation elevated are "very persistent," Cleveland Fed economist Randal Verbrugge wrote in an economic commentary. Verbrugge used a model he developed with Saeed Zaman to analyze price dynamics and where they're heading. The results suggest getting the rest of the way to the Fed's 2% inflation target relies on intrinsic forces, like wage growth and firms changing prices, which take longer to influence the rate of inflation than the simple fading out of extrinsic — or external — shocks.  |