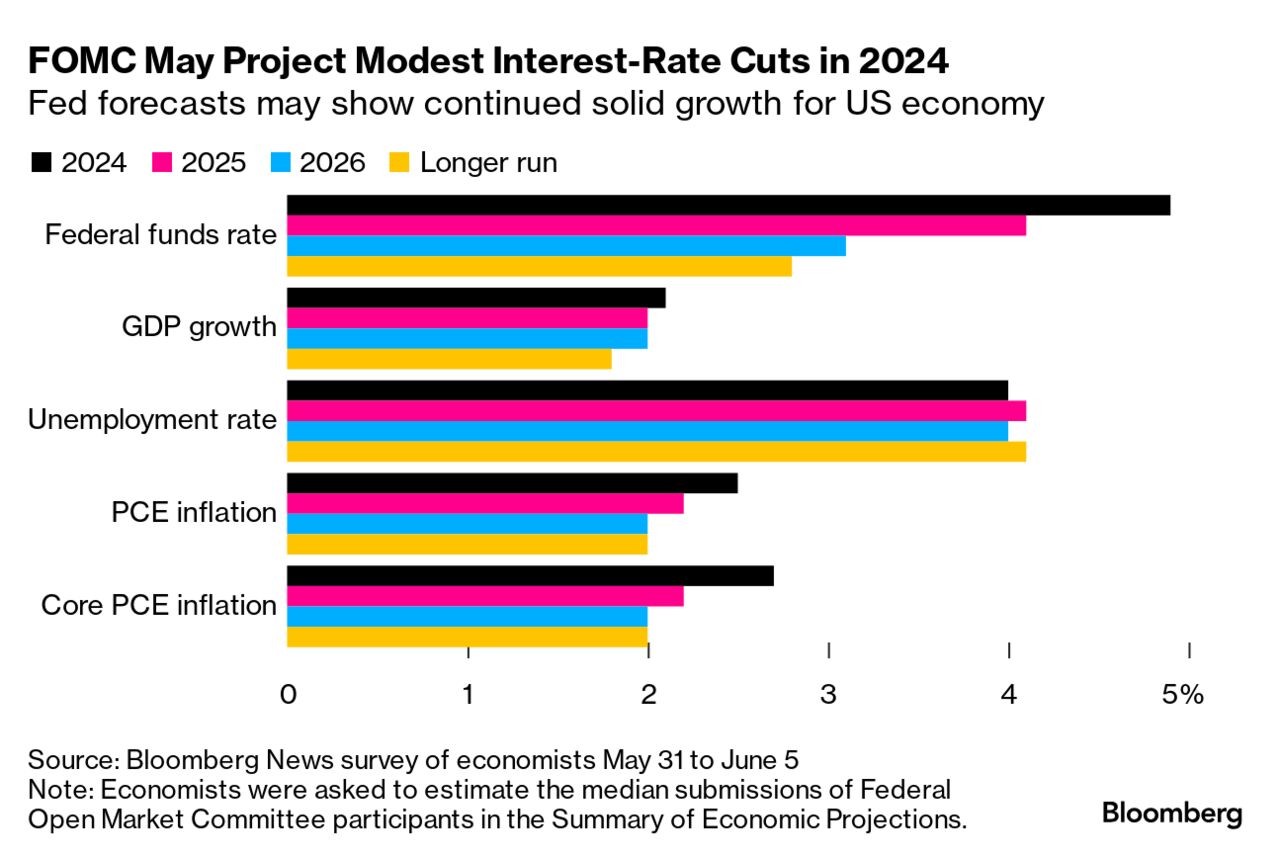

A decade ago, the big question about the Federal Reserve was when the US economic recovery from the worst postwar financial crisis would be strong enough to prompt policymakers to raise interest rates. Today, the debate is a mirror image: When will inflation soften enough to allow policymakers to lower borrowing costs? About this time last year, interest-rate futures indicated confidence the Fed would be cutting rates right now. Instead, the question heading into Wednesday's Federal Open Market Committee policy announcement and Fed Chair Jerome Powell's post-decision press conference is whether there will be any reduction at all by year-end. Inflation is still running closer to 3% than the Fed's 2% target, using policymakers' preferred gauge — the PCE price index. And Wednesday morning's consumer price index, a series that tends to run a little faster than the PCE, is forecast to show inflation stuck around 3 ½%. Fed Governor Christopher Waller, who proved a good gauge of where policy was heading in spring 2022 when he pushed for front-loading bigger-sized rate hikes, last month offered a framework for the timing of lowering rates. "If the data were to continue softening throughout the next three to five months, you can even think about doing it at the end of this year," Waller said of lowering rates. Given that April inflation data were still largely too hot, that means if the May price data do come in softer, that's effectively month-one. "By this framework, a July FOMC rate cut was already pretty much out of the question," Stephen Stanley, chief US economist at Santander US Capital Markets LLC, wrote in a note Tuesday. "If the May results are similar to April's, then there would be no margin for error" with respect to September. The May CPI will also have offered Fed policymakers one last input for their updated projections for the policy rate at year-end. As noted yesterday, economists are divided on whether they'll pencil in two cuts or fewer, down from the three seen back in March.  |