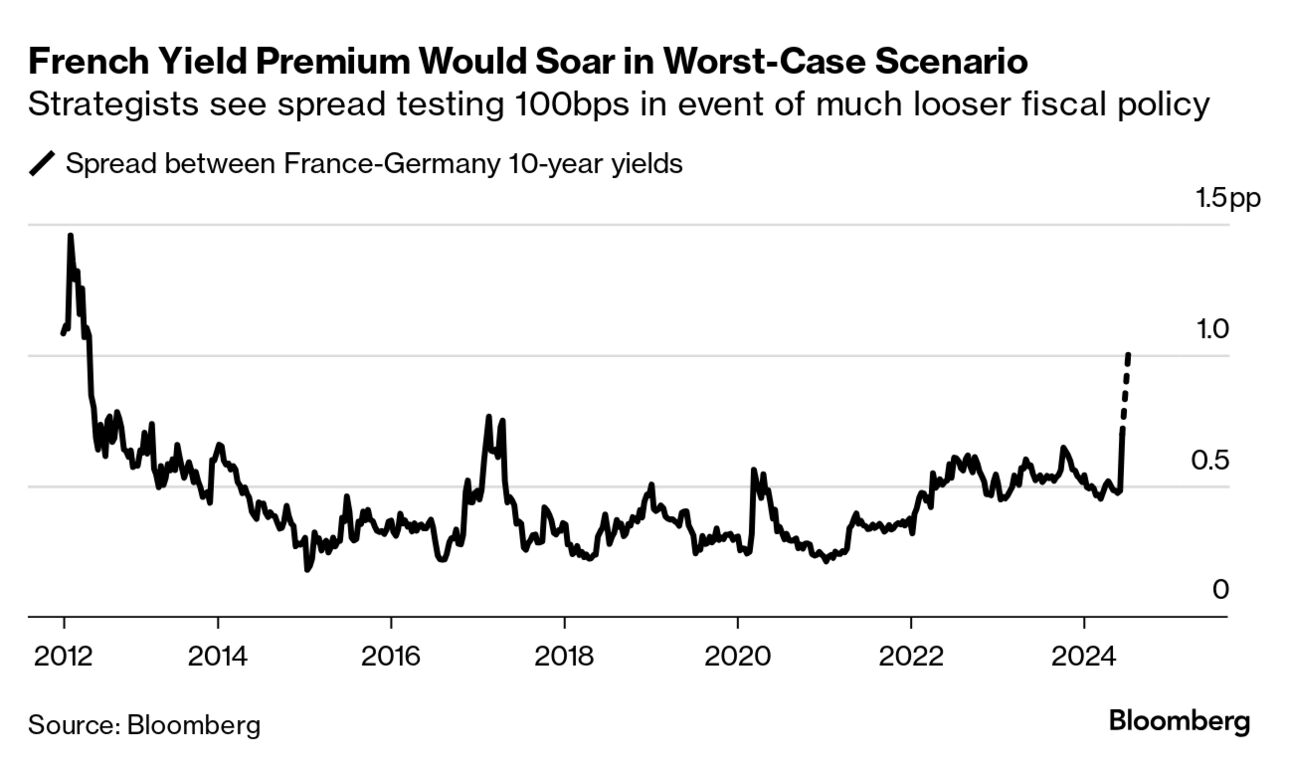

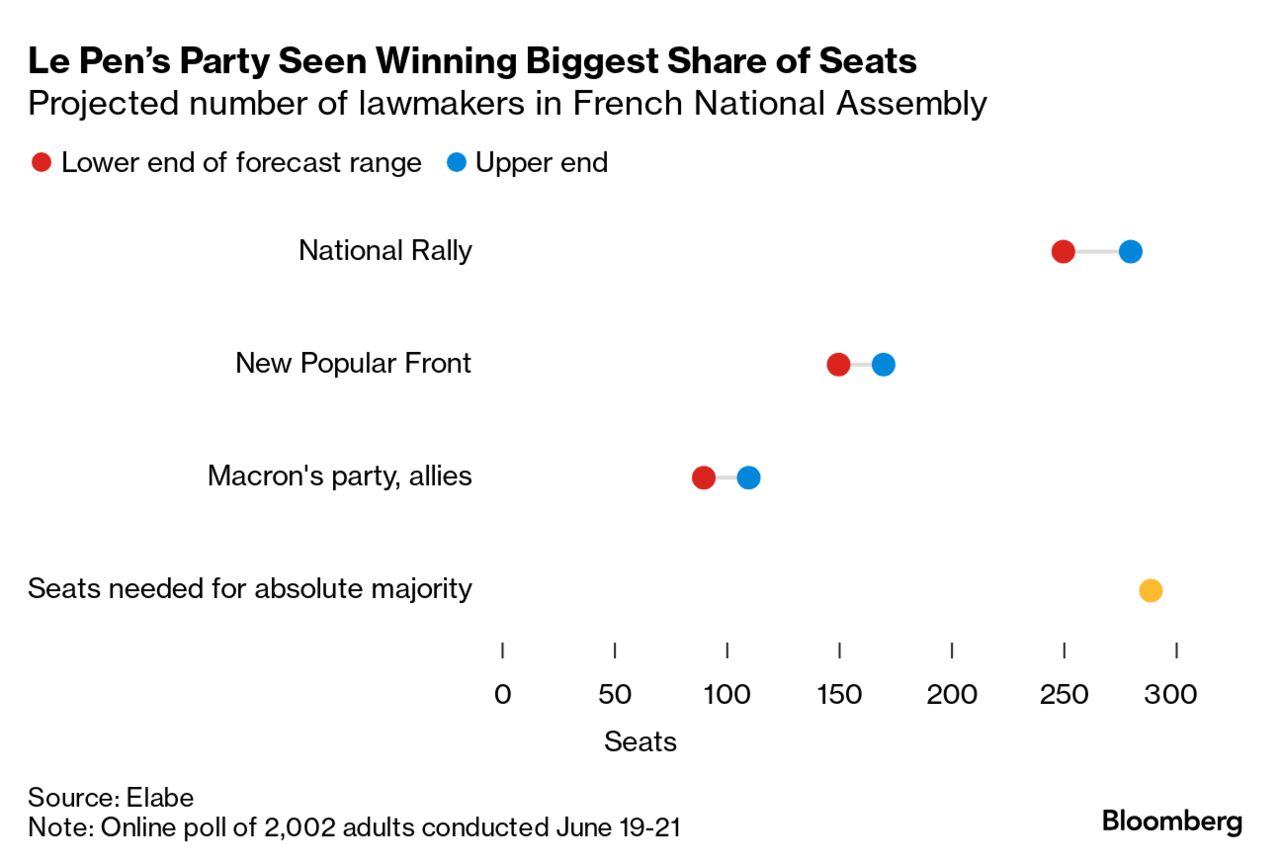

In a year that already featured an exceptional series of elections worldwide, President Emmanuel Macron's snap call for French voters to choose a new parliament still stands out as momentous for markets. The contest to control the National Assembly is one of the most scrutinized in decades. Investors concerned that any winner might swell France's borrowings are now demanding the highest risk premium on its bonds since 2012, and asking if a sequel to Europe's last sovereign debt crisis is imminent. So what might happen in the next couple of weeks — and how would markets react? In our story today, we look at four scenarios: - Shaky Gridlock: the most likely result based on current polling, where Marine Le Pen's far-right National Rally gets the most seats in parliament, but not enough for a majority. Strategists see a higher premium to hold French bonds staying in place under this outcome.

- Awkward Partnership: where the far right clinches enough support to form a government, forcing a so-called "cohabitation" with Macron. The tone taken by the party's leadership would be key for how bonds fare.

- Left Outperforms: where the New Popular Front, the leftist alliance currently running second in polls, somehow wins out on the day. This is the worst-case outcome for bond investors.

- Macron Prevails: currently seen as extremely unlikely, the president's party and allies weather the storm to remain the biggest group in parliament. For bonds, this could be the best outcome.

Currently, the momentum is with Le Pen. The National Rally just increased its lead in Bloomberg's poll of polls, gaining 34.2% against 28.2% for the left. Macron and his allies are lagging in third place. Polls can only signal so much in an electoral system whose design fosters curveballs. France's 577 districts partake in two rounds of voting, and people often choose tactically — for example by switching support between parties to block another from winning. Whatever happens, it's currently hard to envisage an outcome that involves plain sailing, not least at a time when France's debt is above 110% and its big deficits are drawing scrutiny from Brussels. "We see a significant risk of political gridlock and uncertainty, which could result in maintaining market volatility," said Theophile Legrand, a strategist at Natixis. - Get Bloomberg's coverage of the French election in your inbox by signing up to our newsletter, The Paris Edition. Terminal users can sign up here. If you're reading this online, this is the link you need.

- The Bank of Japan discussed raising interest rates on June 14, raising the prospect of a move next month; but the yen remains under pressure.

- China's fiscal revenue shrank at the fastest pace in more than a year, fueling expectations of a rare budget revision to aid the recovery.

- The UK's next government will confront a fresh increase in economic misery levels in its first months in office.

- Ghana reached an agreement in principle with eurobond investors to restructure about $13 billion of debt.

- Sweden's government says that the fight against inflation "has been won."

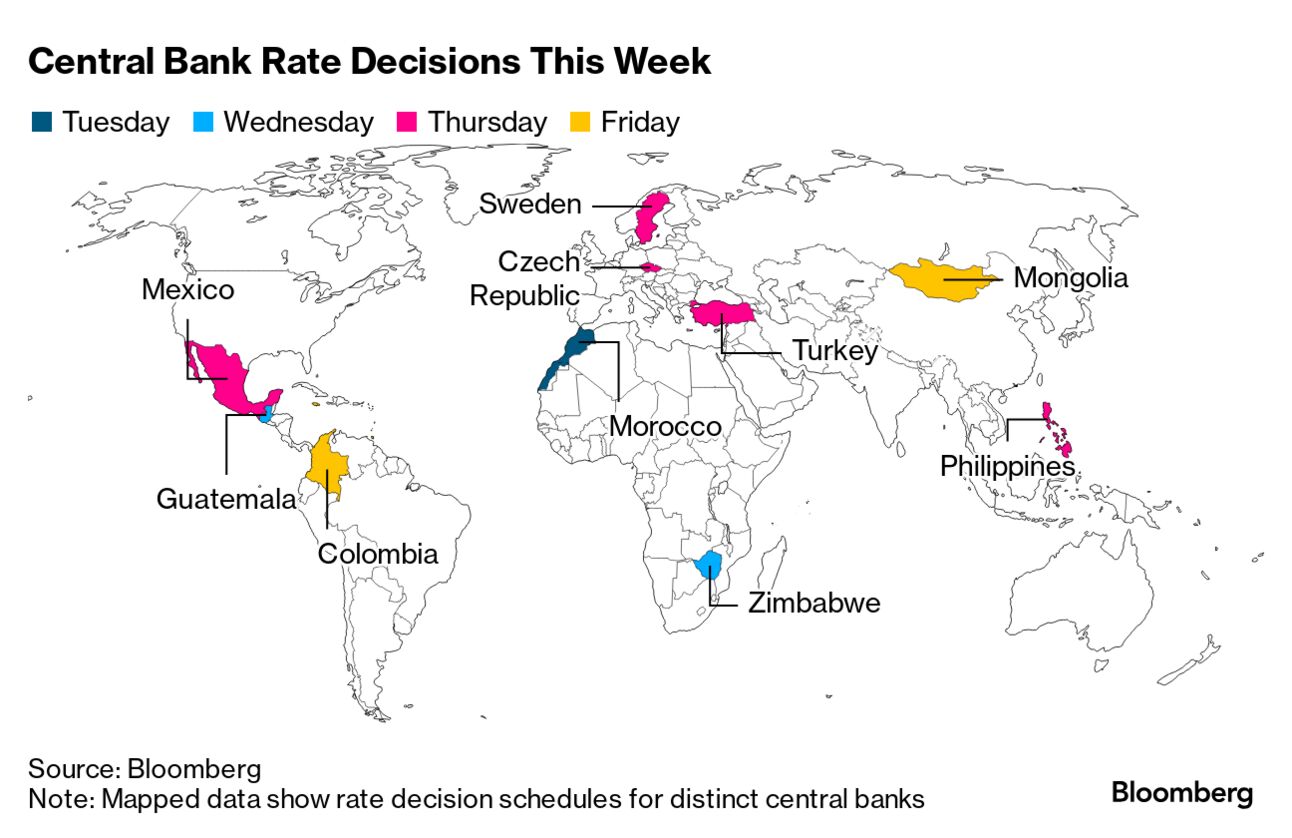

The Federal Reserve's favored inflation yardsticks are poised to show the tamest monthly advances since late last year — a stepping stone for officials to begin lowering rates, possibly as soon as September. Economists expect no change in the May personal consumption expenditures price index and a minimal 0.1% gain in the core measure that excludes food and energy, based on median projections in a Bloomberg survey of economists ahead of data on Friday. Elsewhere, inflation numbers in three major euro-zone economies may also cheer officials, while central banks from Sweden to Mexico will probably keep rates on hold. See here for the rest of the week's economic events. Investment from the US and other high income economies pours into emerging economies during times of quantitative easing by the Fed, according to new research posted by the National Bureau of Economic Research. In a paper titled U.S. Liquid Government Liabilities and Emerging Market Capital Flow researchers found that, by increasing liquidity, QE offers investors more flexibility that their funds can be sold during times of market shocks. "With the assurance that some of their portfolio can be readily sold in liquid markets, rich country investors are more willing to increase investments in illiquid loans to emerging markets," the research paper found. |